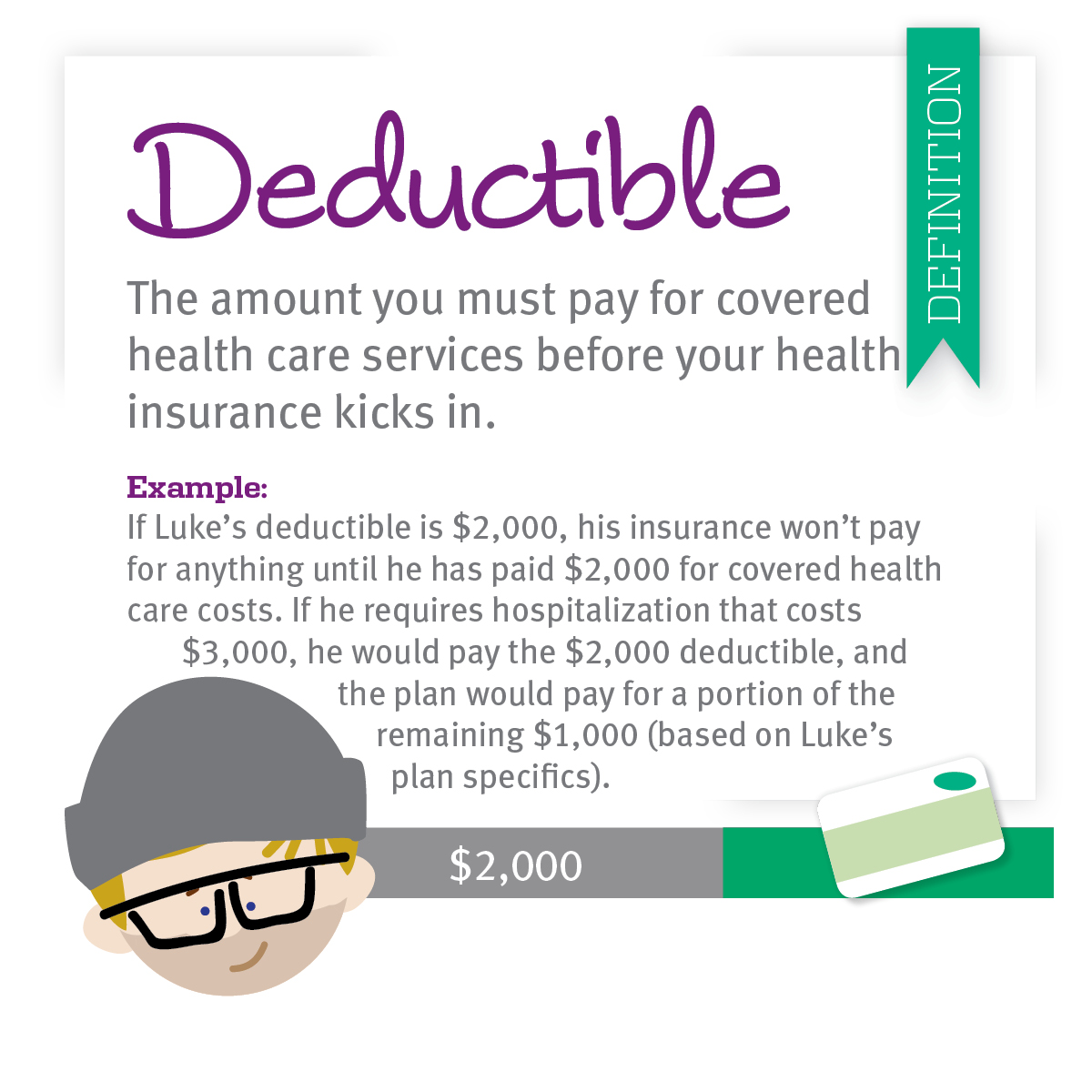

I understand this looks like a strange name and if your organization has nothing to do with the water, it can seem out of place in our conversation. However "inland marine" is the insurance term offered to any company contents that have actually been eliminated from the physical service property itself (What is a deductible in health insurance). Inland marine insurance was originally created to protect products as they were shipped overseas. However, today, these insurance coverage policies cover any goods or contents that are considered "in transit" over water or land, and even, in many cases, those that aren't in actual transit at all. This coverage consists of anything that needs to move from one website to the other, or from your business to your house or to offsite meetingssuch as laptop computers or tablets, cams, lenses and video devices, tools and machines, uncommon art or furnishings, or anything else that your service transportations.

Keep in mind that once business contents are "in transit," or off your residential or commercial property, they are automatically redefined and can no longer be covered as organization individual home. Often insurance coverage companies will set up a "return" feature where they exclude something and then provide a part of minimum protection rather. It's not unheard of for some insurer, for circumstances, to exclude inland marine protection on a standard commercial residential or commercial property policy but then give you as much as $10,000 of company individual residential or commercial property coverage anyway. This is mostly done to try to prevent suits from occurring and cover companies in the case of a small loss.

As an example, let me inform you the story of my landscaper. Before my landscaper was insured with me, he had all of his industrial service residential or commercial property guaranteed through another company. He had a trailer that was filled with expensive backyard equipmentliterally countless dollars of weed eaters, blowers, chainsaws, lawnmowers, toolsthat was stolen. Unfortunately, the person who wrote his initial business home policy did not think about the nature of his business. The theft was not covered under his business residential or commercial property policy since at the time it was stolen, the equipment was more than 100 feet away from his place of organization and he didn't have inland marine coverage.

In all practicality, his "office" is all over town. He works in neighborhoods, and parks, and organization complexes in every location of the Phoenix valley. It's reasonable to state that his devices is hardly ever, if ever, at his actual physical company address. But the industrial home policy doesn't acknowledge by itself the mobile nature of his service. It guarantees just that a person location. The failure remained in the previous agent who didn't ask the best concerns or understand what the landscaper really needed his industrial property insurance to do for him. When you go to get your industrial residential or commercial property insurance coverage make certain you choose a representative who will ask excellent questions, comprehend your scenario, and get you the right coverage for all the activities of https://techmoran.com/2020/03/04/technology-is-changing-the-face-of-real-estate-industry/ your service.

If you take something away, even for work purposes, it's out of its "normal use" and no longer covered. In another case, I have a client who has a business doing interior decoration. She always has great deals of products, home furnishings, and art pieces that she uses to phase, decorate, and stock the areas that she is designing. She purchases the items and owns them up until the tasks are total, and after that the design work and furnishings are sold to her customers. A couple of years earlier, prior to she concerned me for industrial insurance, she moved a $20,000 painting away from her organization premises to use on among her tasks.

Her insurer wouldn't cover it because it was "in transit" and no longer defined as "service personal effects" and she was stuck with the loss. In this location of insurance, and in so many others, it can make a substantial difference to have the right protection when you need it. You are depending on your service to attend to you, your workers and your customers. It is very important that you comprehend all the meanings, coverages, and limitations of a commercial home policy. This knowledge comes through educating yourself and it must likewise come through the extensive work, assessment, and attention to information of an excellent insurance coverage broker.

The Ultimate Guide To How To Get Health Insurance Without A Job

But what is a lot more obvious, is that if the right questions were asked by their insurance coverage business at the time they bought their policies, both of my customers would have been safeguarded from theft and the damage they suffered. Since their representatives did not pay attention to the nature of their work and their true property insurance needs, even believed they had policies, it resembled having no insurance coverage at all. When you go to get insurance coverage for either your individual requirements or for your service, your representative or broker requires to be asking the right questions to make certain you are properly covered. What does homeowners insurance cover.

In these cases, conventional commercial home insurance will be of little or no usage to them. What excellent is having protection if it doesn't ever apply to your circumstances?Remember, as constantly, insurance exists to reduce your dangers. Ensure that your commercial policy properly takes into consideration your actual risks and covers them specifically so that you can reduce any potential losses.

Business auto insurance coverage safeguards small companies when a company-owned automobile is included in an accident, taken, vandalized, or otherwise damaged.Commercial automobile insurance covers damage to a company vehicle and physical injuries when you or a staff member cause a mishap (What is mortgage insurance). Commercial vehicle insurance coverage provides 5 kinds of insurance security: covers legal expenses if someone sues over damage caused by your lorry. for medical bills related to accidents. pays to fix damage to your car from a crash with another vehicle. spends Go to this site for car theft and damage from other causes, such as vandalism. secures you in case a motorist without insurance coverage hurts the motorist or guests in your automobile. Some types of coverage are optional, such.

as crash coverage. Other kinds of coverage are mandated by Click for more info state law. Typically, business-owned lorries by industrial auto insurance. Compare commercial auto insurance prices estimate from top U.S. providers, Business vehicle insurance coverage, likewise called business automobile insurance, just covers business-owned cars. It does not cover individual lorries utilized for organization purposes, unless that's their main use. If your workers use their own vehicles for work errands, they may need worked with and non-owned auto insurance coverage. This policy likewise cover: Items you bring in the car Utilizing the lorry to provide ridesharing through Uber or Lyft Staff member injuries( normally covered through employees' compensation insurance coverage) Occurrences including rented or leased lorries You require commercial auto insurance coverage if your service owns vehicles and uses them to: Travel to and from job sites Transfer tools and equipment utilized for service functions Carry workers or customers Insureon helps small company owners compare quotes from top-rated insurer with one simple online application.